Greetings and Happy Fall!

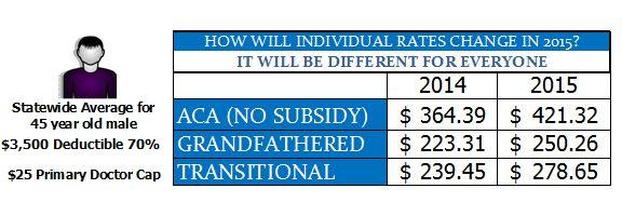

First of all, our sincere appreciation to you for choosing us as your insurance agents and granting us your trust and confidence. We are working hard to provide you updates, answers to your questions and effective coverage during all these changes with health insurance reform. Renewal and Open Enrollment is coming. This week and next, you will be receiving letters from Blue Cross with your rates for 2015. And The Good News Since your plan is: A. Grandfathered - effective before March 10, 2010 or B. Transitional - effective March 11, 2010 to October 1, 2013 You may keep this plan for 2015. The rate increase is based as it has been in the past: 5 year age brackets, cost sharing with local providers and medical expenses paid for everyone in the state having the same plan; but never on your individual medical expenses. So what's next?? Your plan will renew automatically and you will see the change in premium for your coverage starting January 2015. If you do an auto-draft, please make a note of this. The increase seems high - what's up? If we look at the percentage, it is somewhat higher than years past. But if we compare to the new Marketplace plans, keeping your current plan is a very effective value. But what if my situation has changed? Would I get better coverage / premium through The Insurance Marketplace ? You might. This is what we need to do to evaluate. 1. Review our video about the Affordable Care Act so you understand how the new plans and the premium discount tax credit work. 2. Estimate your income for 2015. Put that along with your household size ( as you will report on your 2015 1010 tax return) into the Subsidy Calculator 3. If the premium for the baseline " Silver " plan is substantially lower ( say 40% ), then we may need to evaluate. 4. Remember - if you make a change to your Grandfathered or Transitional plan, you may not change back in the future. This is very important for you folks under 45 whose income may increase in future years. LET US HELP YOU We were very fortunate that last year we were able to help lots of folks get substantial premium saving, upgrade their benefits and in many cases, be able to get the health insurance they really needed for the first time in many years. We have increased staff to help us provide you the answers and support you need. Please call 828-279-4681. Dina Reed is answering this phone. Dina along with Jeannie Blackwelder, Matt Reyna, Jan & Dave will get back to you. In addition, BCBSNC has extended customer service staff and hours. Monday - Wednesday 8 am - 9pm, Thursday & Friday 8am - 10 pm, Saturday 9am-1pm. Call 888-206-4697

0 Comments

As the year comes to a close, folks enrolled in the Marketplace whose projected yearly income falls short of the poverty line ($ 11,490 for single tax filer) are wondering, “What happens next?”

Will the weigh lifted off of their shoulders only come crashing back down again when the numbers don’t match up? In short, no. The Health Insurance Marketplace (HealthCare.Gov) is responsible for determining eligibility for premium tax credits. Due to a Treasury Department rule, if the Marketplace estimates that a person is qualified for a subsidy, they are covered, regardless of year-end actual income. However, individuals whose income rises above 400 percent of the poverty level are required to pay back those tax credits in full.  We are hosting an informational seminar - this Thursday - 10.16 - 6 pm - at Jubilee Community Church, 46 Wall Street, Asheville. Plenty of parking at the adjacent deck.

If interested - please let us know you will be attending. Last fall we took the plunge into Health Insurance Reform - the Affordable Care Act. And- Yes - it was not easy - but we helped over 800 people to review their options, adjust to the changes and for the greater majority - get great insurance at a very affordable premiums. As we come into year two - we are ready again to help you, your family and friends understand these changes and make good decisions for 2015. " Why should I work with you - an insurance agent ? " The answer - " Because this is about insurance ! " We understand the policies, what they cover, the approved networks of doctors working with the insurance companies. How the Marketplace and premium discounts tax credits and increased penalties for 2015 work. And The Best - it costs you NO additional premium.  The Trout Insurance Team gathered to hammer out details for the coming months. Presiding over the gathering was the Trout family's newest edition, Ben!

It has been an eventful summer. We welcome all our new clients whom we enrolled with health insurance through the Affordable Care Act, new insurance companies for home, auto and commercial coverages. We upgraded the websites and welcomed new agents and support staff to serve you. And Most of all - Jan & I welcomed Ben Musial, our first grandbaby. Congratulations to Jennifer and Chris. As we move into the fall, it will be a busy time for us and you. We'll be sending you important information about "New Options, New Plans, New Opportunities" for your insurance coverage. Helping us with easy feedback will allow us to help you very effectively. We welcome your referrals and the opportunity to show you why our motto for now 15 years has been "More Value for Your Insurance Dollar$". Check out our new video below. Many Thanks to Colin, Ralph & Cindy. My homeowners insurance policy reads as though somebody took all of the bad things that can happen in the world and divided them into two buckets: stuff that is covered and stuff that is not covered.

I'm covered for damage from fire, lightning and malicious mischief. I'm covered if a volcano spews lava onto my house. It's right here under "Additional Coverages." Paragraph 10. "Volcanic Action." But there's this other section, "Losses Not Insured," that tells you how insurance really works. For example, Paragraph 2, Subparagraph e: "War, including any undeclared war, civil war, insurrection, rebellion, revolution, warlike act by a military force or military personnel ... " War is what insurers call a correlated risk: If my house gets blown up in a war, it's much more likely that lots of other houses across a wide area are also going to get blown up around the same time. Correlated risks are really hard to insure against. Insurers could go decades without paying anything, then suddenly face more claims than they could ever pay. A lot of the stuff insurers don't cover falls into this category. Earthquakes and floods are both correlated risk. But there's this other category of stuff that insurance companies won't pay for that's not explained by correlated risk. My insurance policy doesn't cover bedbugs — or any kind of bugs, for that matter. Bedbugs, despite what you may have heard on the local news, are not a disaster on the scale of an earthquake. Insurance companies won't cover things like bugs because they don't want to give you an excuse to do ridiculous things. If I had bedbug insurance, I'd furnish my entire apartment from stuff I found on the street. What's the worst that could happen? The fancy term for this is moral hazard. "Moral hazard essentially involves being less careful because you have insurance," says Dan Schwarcz, an insurance expert at the University of Minnesota. "And so, if you have insurance you have less reason to be careful because the insurer will pay for it." Moral hazard turns out to explain one of the most mysterious details in my policy: falling objects. I'm covered for damage from falling objects — trees, satellites, whatever — but only if they first damage the roof or an exterior wall of my building. I kept thinking: What other damage could I have from a falling object? Schwarcz explained it to me: "This coverage excludes scenarios in which there's some falling object in your home, right, that's not caused by an external force. So, let's say that you put your favorite bowling ball right on your shelf and the bowling falls and smashes into your television." Bowling ball breaking the TV: not covered by my insurance policy.  USA Today:

Self-employed give thumbs up to Obamacare Small Business Majority's California Director and Healthcare Policy Director David Chase contributed to an article in USA Today about how the new health insurance marketplaces are helping more people become self-employed and start their own businesses. Entrepreneurs are finding reasonably-priced medical plans through the individual marketplaces that are enabling them to leave their traditional jobs to launch companies, grow their businesses and create new jobs. Years ago, a tenured university professor told me his secret: He was desperate to quit and start his own business. He had enough in savings but didn't dare leave his job. As a man in his mid-50s, he couldn't get health insurance on his own. The Affordable Care Act, which some call Obamacare, was supposed to change that. Supporters said the law would end "job lock" — people stuck in jobs because they couldn't get or afford health insurance elsewhere. Health insurance exchanges offering reasonably priced medical plans would enable entrepreneurs to launch companies, stay in business and create new jobs. COLUMN: Obamacare cures 'job lock' ADVICE: Getting Affordable Care Act subsidies Has the new law worked? For many, the answer is a resounding yes.... READ MORE  The end of summer means many things, such as cooler weather, shorter days and ... the start of football here in Western North Carolina

But most important, it means kids are headed back to school. And that means we all should be extra careful on the roads, in school zones and around buses in Asheville, Hendersonville and surrounding areas. Remember to watch for bikes, too! Here are some tips for both parents and kids to make sure everyone stays safe. Use caution on the roads There are going to be a lot more kids on the sidewalks and streets when school starts, so take it slow and always be aware of your surroundings. That’s good advice for all situations, of course, but be extra cautious around the times when school starts and ends for the day. · Watch out for school zones! They’re usually easy to spot, as many have flashing signs indicating a slower speed limit. · Remember to follow school-bus rules. You aren’t allowed to pass the bus on either side of the road when the red lights are flashing. Even when the lights stop, make sure the coast is clear before moving on. Kids can move quickly and erratically. · Leave yourself extra time to make it to your destination. Whether you’re headed to work or dropping your child off at school, rushing is a recipe for disaster. · Be especially careful in school or child-care parking lots and loading zones! Teach kids to be safe while walking Just a few minutes spent explaining some basic safety rules to your child can help keep them safe when they’re walking to or from school. Young children should never cross streets alone, but if your child is old enough to walk with others, remind them to do the following: · Always use marked crosswalks when crossing streets and look both ways twice. · Do not assume that drivers can see you. Try to make eye contact with them, if possible, when crossing the street. · Watch for driveways when walking on the sidewalk. · Be aware of cars that are turning or backing up. · Never move into the street from behind a car or other obstacle. Don’t chase a ball, pet or anything else into the street. · Always use sidewalks and paths. If there is no sidewalk or path, walk facing traffic and as far to the left as possible. Help them stay safe on their bikes Just as it’s important to help your children learn safety tips for walking to and from school, it’s important to teach bike safety, especially by setting good examples yourself. · Make sure your child wears a properly fitted helmet every time he or she rides a bike. · Before the bicycle is ridden, do a quick inspection to ensure it is working properly and reflectors are in place. · Show your kids how to ride on the right side of the road with traffic and to stay as far to the right as possible. · Encourage your child to walk his or her bike across busy intersections. Or better yet, choose a route without any busy crossroads. · Explain to your child why no one should ride on the handlebars. · Demonstrate the rules of the road by using proper hand signals and obeying traffic signs when you ride bikes together with your child. · Set curfews so your child is not riding a bicycle at dusk or in the dark. · Most importantly, supervise your children every time they ride until you are certain they have good judgment. We know you’re probably familiar with all of these good ideas, but everyone needs reminders. So take it slow, and let’s have a happy and safe school year!  In today’s economy, everyone is pinching pennies. So why worry about umbrella coverage? Shouldn’t a home and auto policy leave you adequately covered?

Unfortunately, we live in a world of lawsuits. Large damages can be awarded, be extremely expensive and have long-term financial impact. Those lawsuits can come from unlikely sources, such as our furry friends. Take Herschel for instance. Herschel is a much-loved, rather timid labradoodle who enjoys taking naps on the driveway while his owner mows the lawn. Herschel watched from eight feet away as his neighbor, a 39 year old man, showed off his rollerblading skills to his kids. The man wiped out on the sidewalk in front of Herschel’s house and broke his leg. He required surgery, costing around $35,000 in medical costs and $18,000 in lost wages. Fair or not, the man brought a lawsuit against Herschel’s owner, suing for $220,000 in damages. He alleged that Herschel had caused the accident by getting in his way, despite multiple witnesses to the contrary. But Herschel’s owner was lucky--a jury vindicated Herschel. However, lawsuits such as these can easily exceed the limits on a homeowner’s policy, leaving the insured responsible for the remainder. An umbrella policy would prevent that, giving you an extra $1 million to $5 million in coverage. Our furry friends can put your assets at risk in other ways as well. According to the Center for Disease Control and Prevention, 4.7 million people are bitten by dogs each year, with half of those occurring on the owner’s property. Dog bites, according to the Insurance Information Institute, account for about a third of all homeowner’s insurance claims, which only cover limited damages. Protect what you love. Call us to talk about your umbrella options. |

Dave Trout

|

-

Insurance

- Trout Team

-

Resources

- Join The Team

- Employee Success

- Fixing the ACA "Family Glitch"

- Aetna/CVS Health NC

- Medicaid Expansion

- Client Center

- Newsletter

- Reviews

- Blog

-

Articles

>

- Health Insurance 2022

- Friday Health

- Comparing 2022 Plans

- Insurance Partners

- Best Value Insurance Plans

- ARP Facts CMS

- ARP Unemployment

- ARP 2020 Excess Premium Subsidy

- No Income Cap

- Unemployment Glitch

- Asheville Homesharing

- 2019 Verification-a

- BCBS Online Setup

- APTC Income 2023 & Tax Form 1040

- Lost Subsidy

- Privacy Policy

-

Community

- Understanding Medicare 2024

- Weaverville Primary Spring Fling

- Alignment's 5-Star Switch

- Employer Networking w/ Just Economics

- FALLing with Families

- Blue Ridge Pride Festival

- Goombay & YMI

- YMI Winter Coat Drive

- Medicare Seminar

- Art in Autumn + MANNA

- Music on Main

- Western Women's Business Center Conference

- Mural on Main Street

- Expanded Team- Next Generation

- Back to School

- Weaverology

- Mother Earth Food

- Contact Us

RSS Feed

RSS Feed

“We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or call 1.800.Medicare to get information on all of your options.”

Trout Insurance is an independent authorized agency licensed to sell and promote products from Blue Cross and Blue Shield of North Carolina (Blue Cross NC). The content contained in this site is maintained by Trout Insurance. Blue Cross and Blue Shield of North Carolina is an independent licensee of the Blue Cross and Blue Shield Association. ®, SM Registered marks of the Blue Cross and Blue Shield Association.”

|

|

-

Insurance

- Trout Team

-

Resources

- Join The Team

- Employee Success

- Fixing the ACA "Family Glitch"

- Aetna/CVS Health NC

- Medicaid Expansion

- Client Center

- Newsletter

- Reviews

- Blog

-

Articles

>

- Health Insurance 2022

- Friday Health

- Comparing 2022 Plans

- Insurance Partners

- Best Value Insurance Plans

- ARP Facts CMS

- ARP Unemployment

- ARP 2020 Excess Premium Subsidy

- No Income Cap

- Unemployment Glitch

- Asheville Homesharing

- 2019 Verification-a

- BCBS Online Setup

- APTC Income 2023 & Tax Form 1040

- Lost Subsidy

- Privacy Policy

-

Community

- Understanding Medicare 2024

- Weaverville Primary Spring Fling

- Alignment's 5-Star Switch

- Employer Networking w/ Just Economics

- FALLing with Families

- Blue Ridge Pride Festival

- Goombay & YMI

- YMI Winter Coat Drive

- Medicare Seminar

- Art in Autumn + MANNA

- Music on Main

- Western Women's Business Center Conference

- Mural on Main Street

- Expanded Team- Next Generation

- Back to School

- Weaverology

- Mother Earth Food

- Contact Us